%20(2)_edited.png)

A Practical Guide to Internal Controls for Fraud Prevention

- Marketing Team

- Dec 15, 2025

- 15 min read

Updated: Dec 15, 2025

Internal controls are the bedrock of fraud prevention. They’re the specific policies, procedures, and systems you put in place to protect your company’s assets, keep your financial reporting honest, and shut down opportunities for fraud.

Think of it as a proactive defense system. This isn't about ticking compliance boxes; it’s about building a strategic framework that guards your organization from the inside out. This is bigger than just stopping theft—it’s about creating a resilient business built on a foundation of trust and integrity.

Why Internal Controls Are Your First Line of Defense

In a world of increasingly sophisticated threats, waiting to react is a recipe for disaster. If you're waiting until fraud has already happened, you've already lost money, damaged your reputation, and are now facing a brutal, often incomplete, recovery process. The financial reality is stark and unforgiving.

A recent report drove this point home, revealing that a staggering 79% of organizations were hit with payments fraud attacks in 2024. The number one culprit? Business email compromise (BEC)—a type of attack that directly preys on weak internal controls.

Worse yet, the chances of getting your money back are plummeting. Only 22% of businesses managed to recover a significant portion of their losses. You can get the full story on this alarming trend in the complete payments fraud survey.

This data screams one clear message: strong internal controls for fraud prevention are no longer a "nice-to-have." They are absolutely essential for survival and growth.

More Than Just a Safety Net

Viewing internal controls as just a safety net misses the bigger picture entirely. When done right, they become a strategic asset that delivers real business advantages. A well-designed system creates a culture of accountability and transparency that filters down through every single level of the organization.

It all starts with a rock-solid ethical foundation. When leadership is genuinely committed to integrity, it sets a powerful tone that influences employee behavior far more than any policy manual ever could. You can dig deeper into cultivating this critical element by exploring the importance of setting the right tone from the top.

A well-designed framework brings clarity, cuts down on ambiguity, and empowers employees to make the right call. This foundation builds trust not just with your team, but also with investors, customers, and regulators. It’s a clear signal that your organization is well-managed, reliable, and serious about protecting its assets and its good name.

The Core Pillars of a Strong Framework

Before we get into the nitty-gritty, it helps to understand the high-level view. Every effective internal control system is built on a handful of core pillars. These components work in tandem to create a layered defense that addresses different risk points across your operations. Getting these pillars right is the first step to building a system that truly protects your business.

Here's a quick breakdown of those foundational components.

Key Pillars of an Internal Control Framework

Pillar | Description | Example Control |

|---|---|---|

Control Environment | The ethical tone and integrity standards set by leadership that influence the entire organization. | A formal code of conduct that is consistently enforced and communicated from the top down. |

Risk Assessment | The process of identifying, analyzing, and managing risks relevant to the organization's objectives. | Conducting regular fraud risk assessments to identify new vulnerabilities in payment processes. |

Control Activities | The specific policies and procedures implemented to mitigate identified risks. | Enforcing segregation of duties, where one person cannot both approve and issue a payment. |

Information & Communication | The systems used to capture and exchange information needed to conduct, manage, and control operations. | Clear reporting channels, including a secure and anonymous whistleblower hotline. |

Monitoring Activities | The ongoing evaluation of internal control performance to ensure they are effective and working as intended. | Performing periodic reconciliations of bank accounts and internal financial records. |

Think of these five pillars as the essential building blocks. When they are all strong and working together, you create a structure that is far more resilient to the evolving threats that businesses face today.

Designing Your Control Framework from the Ground Up

Building a system of internal controls that actually stops fraud isn't about downloading a generic template and hoping for the best. Forget the one-size-fits-all approach. Think of it more like a tailor crafting a custom suit—it has to be shaped to your company’s specific operations, risks, and culture.

Sure, established models like the COSO framework offer a great starting point. They give you the principles. But your job is to adapt those principles into a practical defense system that works for your business, whether you're a lean startup or a global corporation. The goal is always the same: create a structure that makes fraud hard to pull off and easy to spot, without grinding your daily operations to a halt.

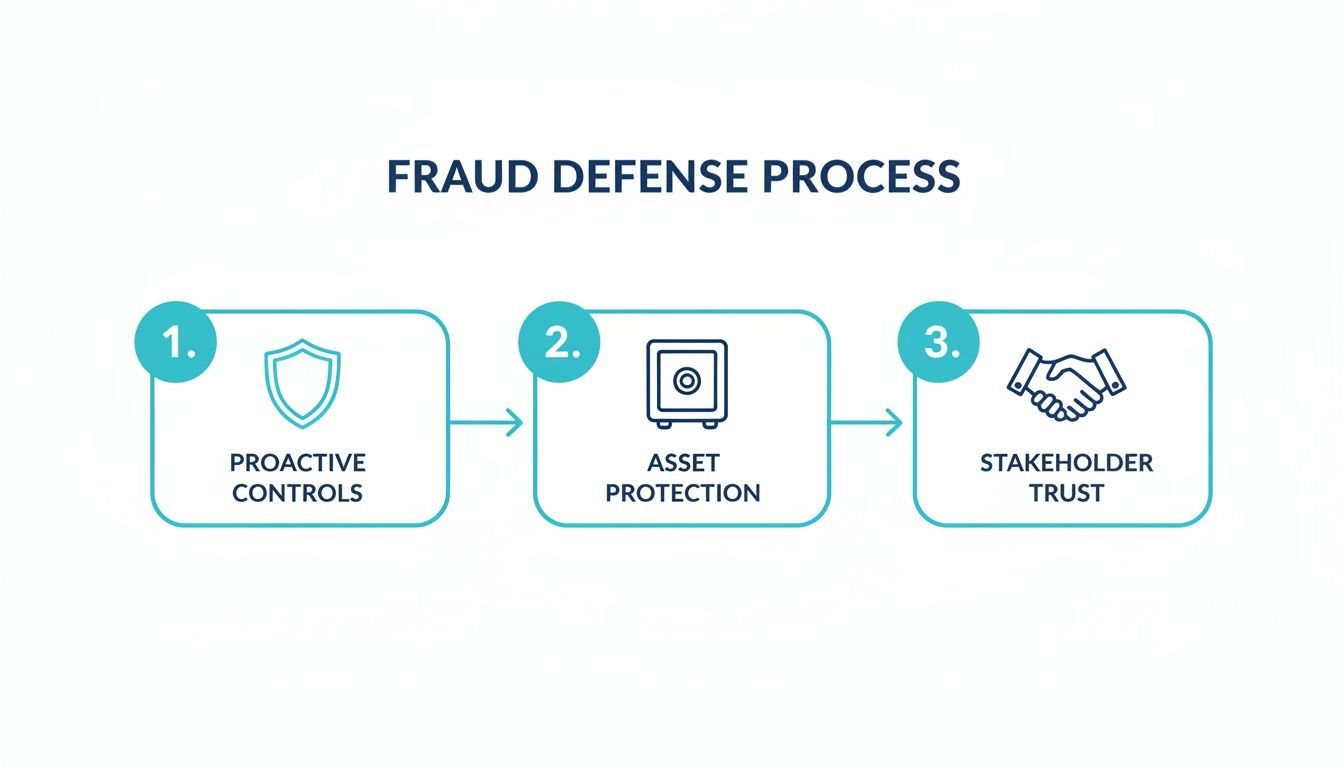

This process turns abstract ideas into a tangible defense. As you can see below, proactive controls are the foundation that leads directly to protecting your assets and, ultimately, strengthening stakeholder trust.

Each element here builds on the last. It’s a resilient structure where your internal integrity directly supports the outside world’s confidence in your organization.

Conducting a Practical Risk Assessment

Your journey has to start with an honest, thorough risk assessment. This is where you get real about the specific fraud schemes that could actually hit your business. A tech company’s biggest headaches might be data theft and intellectual property leaks. A retailer, on the other hand, is probably more worried about inventory disappearing or bogus customer returns.

Let’s make this tangible with two completely different scenarios:

SaaS Startup Billing Cycle: The risk here isn't someone walking out with a laptop; it's revenue leakage. Imagine a single employee has the power to issue customer credits, create discount codes, and adjust subscription terms without any oversight. That's a huge vulnerability. It creates a perfect opportunity to give "free" service to friends or even get kickbacks.

Manufacturing Procurement Process: For a manufacturer, the weak spots are often in the supply chain. A procurement manager who can add new vendors, approve their invoices, and authorize payments is a major red flag. This setup opens the door for them to create fake shell companies and pay fraudulent invoices for goods that never existed.

By mapping out your core business processes step-by-step, you can quickly find these weak spots where a lack of oversight is just asking for trouble.

Fostering a Strong Control Environment

Let’s be clear: policies and procedures are useless without the right culture. The control environment is the ethical foundation of your entire framework. It's the "tone at the top" that shows everyone how seriously the organization takes integrity.

When leadership consistently acts with and enforces ethical behavior, that attitude cascades through the whole company. It influences employees far more than any rulebook ever could.

A weak control environment can completely undermine even the most brilliantly designed policies. If employees see leaders bending the rules or putting results ahead of ethics, they’ll learn fast that the controls are just for show.

You build this environment with clear communication and consistent enforcement of the rules for everyone—especially senior management. It means hiring for integrity and creating a place where people feel safe enough to ask questions or report concerns without fearing retaliation.

Designing Controls That Empower, Not Obstruct

The final piece is to design specific control activities that shut down the risks you’ve found. The key is to create checks and balances that are effective but not so clumsy that they kill productivity. Good controls should feel like guardrails, not roadblocks.

Here are a few practical examples of controls tailored to our scenarios:

For the SaaS Startup: You could implement a system where creating a new discount code requires approval from a manager in a completely different department, like finance. On top of that, you’d run monthly reports that automatically flag any accounts with unusually high credits or discounts for a closer look.

For the Manufacturer: Enforce a strict segregation of duties. The person who adds a new vendor to the system should never be the same person who can approve that vendor’s invoices. You could also require dual signatures for any payment over a certain threshold, like $10,000.

These controls aren't random; they directly address the specific vulnerabilities we identified earlier. By focusing your energy on high-risk areas and building practical, targeted checks, you create a robust framework that protects your assets while letting your business run smoothly.

Weaving Critical Preventive Controls Into Your Daily Operations

A fraud prevention framework on paper is just a plan. The real work starts when you weave those controls into the very fabric of your daily operations. This is where you move from theory to tangible actions that actively shut down opportunities for misconduct. The goal isn't to create more bureaucracy; it’s to build these safeguards so seamlessly into your workflows that they become second nature.

Getting this right means being deliberate and strategic, focusing on your highest-risk areas first. A solid internal control framework has to prioritize robust strategies for eliminating data breach risks in BFSI, since stolen data is often the first step in a much larger fraudulent scheme. You'll find that the most powerful preventive controls are often the simplest in concept, but demand the most discipline to execute.

Segregation of Duties: The Cornerstone of Prevention

If there’s one principle at the heart of any effective system of internal controls for fraud prevention, it’s Segregation of Duties (SoD). It’s a simple but profoundly powerful idea: no single person should have control over two or more conflicting parts of a process. This one control makes it incredibly difficult for fraud to happen without collusion, which dramatically increases the risk of getting caught.

Think of it like needing two different keys to open a company safe. One person holds the key to initiate a transaction (like creating a purchase order), another has the key to authorize it (a manager’s approval), and a third holds the key to record it (the bookkeeper).

The core idea behind SoD is to eliminate the opportunity for one person to both commit and conceal fraud. When duties are properly segregated, an employee would need an accomplice to bypass the system, making the act far more difficult and risky.

This is your number one defense against common occupational frauds, from creating fake vendors to manipulating payroll.

Putting SoD Into Practice

Applying SoD means taking a hard look at your key operational cycles. Here’s a tactical checklist for implementing this principle where it matters most:

Accounts Payable: * Separate Vendor Setup from Invoice Processing: The person who can add a new vendor to your system should never be the one who processes or approves that vendor's invoices. This is how you stop the creation of shell companies for fraudulent payments. * Divide Payment Initiation and Authorization: The employee who enters invoices and prepares a payment run must not have the authority to approve or release the final payment. This creates a critical checkpoint.

Payroll Management: * Isolate HR and Payroll Functions: The individual who adds a new employee or changes pay rates in the HR system should not be the same person who processes the payroll. This simple control stops the creation of "ghost employees." * Require Independent Review: Have a senior manager—someone completely separate from the payroll processing function—review the final payroll register before any funds are disbursed.

Inventory and Asset Management: * Separate Physical Custody from Record-Keeping: The warehouse manager who oversees the physical stock can't be the same person who updates inventory records in the accounting system. This control helps prevent inventory theft from being hidden by simply adjusting the books.

To give you a clearer picture, here are some practical examples of how SoD looks across different departments.

Segregation of Duties Examples Across Departments

The table below breaks down how you can apply the principle of Segregation of Duties to prevent fraud in common business functions. Each row shows how to split the custody of an asset, the authorization of an action, and the recording of the transaction among different people.

Department | Task to Separate 1 (Custody/Execution) | Task to Separate 2 (Authorization) | Task to Separate 3 (Record-Keeping) |

|---|---|---|---|

Finance & Accounting | Employee who handles cash receipts and deposits. | Manager who approves write-offs or credits. | Accountant who reconciles the bank statements. |

Sales | Salesperson who initiates a customer order. | Sales manager who approves special pricing or discounts. | Accounting clerk who records the final sale in the ledger. |

Procurement | Employee who receives goods from a supplier. | Department head who approves the purchase requisition. | Accounts Payable clerk who enters the supplier invoice. |

Human Resources | HR admin who onboards a new employee. | Hiring manager who authorizes the job offer and salary. | Payroll specialist who processes the new hire's first paycheck. |

Implementing these separations is a fundamental step in creating a control environment where fraud is not just discouraged, but actively blocked by the process itself.

Beyond SoD: Other Essential Preventive Controls

While SoD is foundational, a truly layered defense requires a few other critical controls working together. These measures create extra checkpoints that reinforce accountability and reduce temptation. For a deeper dive, our guide on how to prevent employee theft offers more strategies.

First, implement robust authorization protocols. This means establishing clear, tiered approval limits for expenditures. For example, any purchase over $5,000 might require a manager’s signature, while anything over $50,000 needs director-level approval. This ensures that significant transactions always get the right level of scrutiny.

Finally, never overlook the human element. Thorough pre-employment background checks are a fundamental preventive control. Verifying past employment, checking references, and conducting criminal background checks (where legally permissible) can help you filter out individuals with a history of fraudulent behavior before they ever walk through your door.

Leveraging Detective Controls and Technology for Early Warning

While preventive controls are your first line of defense, they aren’t foolproof. A determined fraudster will always look for a way around them, which is why a robust detection layer is non-negotiable.

This is where you shift from building walls to installing a highly sensitive alarm system. You’re using technology as a vigilant watchdog to get those crucial early warnings.

Effective detective controls go way beyond a simple monthly bank reconciliation. We're talking about continuous, automated monitoring that can spot anomalies as they happen, not weeks or months after the fact. This proactive detection is also a powerful deterrent, sending a clear message that any funny business will be caught quickly.

This kind of system is designed to flag suspicious activities in real time. The key here is the ability to pull multiple data points into a single view, allowing a human analyst to spot patterns that would otherwise be completely lost in the noise of daily transactions.

Harnessing AI for Anomaly Detection

Modern fraud detection is increasingly powered by artificial intelligence and advanced analytics. These systems can analyze thousands of transactions in seconds, flagging deviations from normal patterns that a human would almost certainly miss. This is a game-changer for internal controls for fraud prevention.

Think about these real-world applications:

Unusual Payment Times: An AI model can learn your company's typical payment schedule and immediately flag an invoice payment processed at 2:00 AM on a Sunday.

Duplicate Invoice Numbers: The system can automatically cross-reference all incoming invoices, flagging any duplicates or those from unapproved vendors before payment is released.

Behavioral Biometrics: For customer-facing fraud, technology can analyze how a user interacts with your platform—their typing cadence, mouse movements, or how they navigate a page—to detect signs of account takeover.

This isn't about surveillance; it's about using privacy-preserving AI to spot statistical outliers. Such tools are becoming essential. As consumer fraud losses in the US soared past $12.5 billion in 2024, the need for better detection has become critical. With deepfake technology now responsible for 1 in 20 identity verification failures, old methods just don't cut it anymore.

The Critical Human Element

Technology is a powerful ally, but it doesn't replace the human element—it enhances it. Your employees are often the first to notice when something feels off. Fostering a culture where they feel safe and empowered to speak up is one of the most effective detective controls you can have.

This is where a secure, anonymous whistleblower hotline becomes invaluable. An effective program ensures that employees can report suspicious activity without fear of retaliation. Tips are a leading source for uncovering occupational fraud, but only if the reporting mechanism is trusted and accessible.

A whistleblower program's success hinges entirely on trust. If employees believe their concerns will be ignored or, worse, that they will face negative consequences for reporting, the hotline becomes useless. Anonymity, clear follow-up procedures, and a strict anti-retaliation policy are the pillars of a program that works.

This combination of advanced technology and an engaged workforce creates a formidable detection layer. For organizations looking to explore this further, understanding the capabilities of machine learning in fraud detection is a crucial next step in building a resilient defense.

Finally, unannounced audits and spot checks remain a timeless and effective detective control. The unpredictable nature of these reviews keeps everyone on their toes and disrupts any fraudulent schemes that rely on predictable oversight schedules. Leveraging detective controls and advanced technology is paramount for early warning, including exploring AI-driven signature verification for fraud analysis, driven by increasing regulatory pressure. By combining these technological and human-centric strategies, you build a system where fraudsters know they have nowhere to hide.

Sustaining and Adapting Your Controls for Long-Term Resilience

Getting a strong set of internal controls for fraud prevention in place is a massive win, but let's be clear—it's only halftime. The business world is always in motion, and fraud tactics evolve even faster. A control system that was airtight last year could be riddled with holes today if you just leave it alone.

This is where so many programs fail. Sustaining your controls means treating them like a living system, one that needs regular attention and adaptation to stay effective. This isn't about clinging to outdated rules; it's about building a resilient fraud prevention program that can bend without breaking.

From Static Rules to a Dynamic Defense

The single biggest mistake I see companies make is treating their controls like a one-and-done project. They write a brilliant manual, file it away, and assume the job is finished. That "set it and forget it" mindset is practically an open invitation for trouble.

To build any kind of long-term resilience, you have to commit to a cycle of continuous improvement. This means regularly pressure-testing your controls to make sure they’re still working as intended and haven't been quietly bypassed by clever workarounds or simple process changes.

Controls degrade over time. It's inevitable. Processes shift, new tech gets rolled out, and employees find shortcuts. Without consistent testing, you're operating on the dangerous assumption that your defenses are still up.

A proactive approach isn't just a good idea; it's the only way to ensure your internal controls for fraud prevention stay relevant against the threats you'll face tomorrow, not just the ones you faced yesterday.

Conducting Regular Control Self-Assessments

One of the most practical ways to keep a finger on the pulse is through control self-assessments (CSAs). This process is brilliant because it empowers department heads and process owners to actually review and validate the controls in their own backyard. It shifts control management from a top-down mandate into a shared, operational responsibility.

When a weakness is identified, the response needs to be swift and decisive. The goal isn't to point fingers but to get to the root cause and implement real corrective actions.

Was the control poorly designed from the start?

Did a recent software update make it obsolete?

Is more employee training the real answer?

Answering these questions turns a control failure from a liability into a valuable learning opportunity, making your entire framework stronger in the process.

Ongoing Training and Adapting to New Realities

Your people are your single most critical control asset, but only if they're kept in the loop. Ongoing education is non-negotiable for keeping everyone aware of new threats, especially the sophisticated phishing and Business Email Compromise (BEC) scams designed to exploit human trust.

Training has to be practical. Use real-world examples to show how fraud happens and what their specific role is in shutting it down. And as your business changes, your controls have to change with it. Just think about these common shifts:

Shifting to remote work introduces a whole new set of risks around data security and virtual approvals.

Expanding into new markets means navigating completely different regulatory environments and fraud patterns.

Adopting new technologies like AI or automation demands a full re-evaluation of the process controls you've relied on for years.

This kind of adaptability is now a global imperative. The 2025 Global Fraud Index reveals how control frameworks must respond to international trends. Europe leads with 13 of the 15 most-protected nations, largely thanks to regulations like the EU's PSD3, which places scam liability directly on institutions. This trend mirrors Australia's Scam Prevention Framework, which requires banks and telecoms to take ‘reasonable steps’ to stop fraud.

This global shift toward 'failure to prevent' initiatives puts the pressure squarely on organizations to constantly enhance their controls. You can explore how these global trends are shaping the future of fraud prevention and the role of AI in the full report.

Common Questions About Internal Controls for Fraud Prevention

When you're in the trenches building out your fraud defenses, practical questions always come up. Let's dig into some of the most common ones we hear from leaders trying to strengthen their framework.

Aren't Robust Controls Only for Big Corporations?

Not at all. While you might not have the budget for a sprawling internal audit department, the core principles of internal controls for fraud prevention are completely scalable. It's all about focusing on high-impact, low-cost measures.

Segregation of duties is a perfect example. Even if your finance team is just two people, you can still separate critical tasks. One person approves invoices, the other executes the payments. It's that simple. Another powerful, cheap control is mandatory vacations—having someone else cover a role for a week or two is an incredibly effective way to uncover irregularities.

The goal isn't to build a massive corporate bureaucracy. It's about applying the principles—like separation and oversight—in a way that fits your reality. A few small, consistent checks are far more powerful than a complex system nobody uses.

Are Automated Controls Really Better Than Manual Ones?

Both have their place, but automation gives you a massive advantage in consistency and reliability. Manual controls depend on human diligence, and people get busy, distracted, or simply make mistakes. An automated control, like a system-enforced approval workflow, runs perfectly every single time.

Think about it this way: instead of relying on a manager to manually scrutinize every single expense report, an automated system can instantly flag any submission that violates policy or is missing a receipt. This doesn't get rid of human judgment; it frees it up to focus on the exceptions that truly matter.

How Often Should We Be Testing Our Controls?

Internal controls are not a “set it and forget it” exercise. Things change, processes evolve, and people come and go. At a bare minimum, you need to conduct a comprehensive review of your entire control framework annually.

But for high-risk areas, you need to be more vigilant.

Quarterly Reviews: Perfect for the most critical processes like payroll, accounts payable, and cash handling.

Event-Triggered Reviews: Absolutely essential after a major business change, like implementing new software, entering a new market, or experiencing significant staff turnover.

Regular testing ensures your defenses stay relevant and effective. It helps you find the weak spots before they can be exploited, turning your controls from a static wall into an adaptive shield that actually works.

Ready to build a proactive, ethical defense against internal risks? Logical Commander Software Ltd. provides an AI-driven platform that identifies early warning signals of fraud and misconduct without invasive surveillance. See how our E-Commander platform can unify your risk management efforts. Learn more and protect your organization.