%20(2)_edited.png)

A Guide to Internal Controls to Prevent Fraud

- Marketing Team

- Jan 3

- 15 min read

Updated: Jan 5

Weak or nonexistent internal controls to prevent fraud aren't just a line item on an audit report. They are a direct threat to your financial health, operational stability, and corporate reputation. For decision-makers in Compliance, Risk, and Legal, this isn't a theoretical problem—it's a direct challenge to governance and a significant source of business liability. When organizations fail to implement and enforce these controls, the consequences are tangible, expensive, and often devastating.

The High Cost of Ineffective Fraud Prevention

When internal controls are treated like a compliance checkbox instead of a strategic necessity, you leave the door wide open for serious business impact. The financial damage from fraud goes far beyond the initial theft; it triggers a ripple effect of investigation costs, legal fees, regulatory fines, and a severe erosion of trust from stakeholders. This is a problem that reactive forensics and post-incident investigations cannot solve. The data paints a stark picture of a widespread threat where prevention is the only viable strategy.

A recent survey found that a staggering 79% of organizations worldwide were hit by payments fraud attacks or attempts. That number confirms that fraud is not a rare event but a persistent, daily operational threat driven by the human factor. To make matters worse, the ability to recover stolen funds is alarmingly low and continues to decline. Discover more insights on payments fraud trends.

The Human Factor and Low Recovery Rates

The challenge grows exponentially when you recognize that most fraud schemes originate from insider risk—the human factor. This can range from malicious intent to unintentional errors, but both exploit weaknesses in manual processes. Bad actors are experts at finding these gaps, while even well-meaning employees can make costly mistakes without proper, non-intrusive oversight.

The business impact is crystal clear:

Plummeting Recovery: Only 22% of organizations successfully recovered 75% or more of the funds they lost to fraud.

Widespread Losses: A majority of businesses (58%) recovered less than three-quarters of their losses, meaning most of the stolen money is permanently lost.

These numbers highlight the critical failure of reactive, after-the-fact responses. Waiting to act until after a fraudulent event is a losing strategy. The cost of forensic accounting, legal battles, and internal investigations often dwarfs the amount of money you might eventually recover.

Relying on post-incident investigations is like installing an alarm that only goes off after the burglars have left. The damage is done, the liability is real, and your chances of a full recovery are slim. Proactive prevention is the only sound business approach.

A Necessary Shift in Mindset

This reality demands a fundamental shift from a reactive to a proactive mindset. Effective internal controls to prevent fraud must be designed to stop incidents before they happen, not just to document them afterward. This means moving beyond manual checks and periodic audits—which are easily sidestepped—and toward systems that provide continuous insight into potential human-factor risks.

The only sustainable path forward is one that puts prevention first, addressing insider risks at their source before they can spiral into financial and reputational disasters. This preventive approach isn't just good business—it's the new standard of ethical, AI-driven risk management.

Understanding The Core Components Of Internal Controls

To build a real defense against internal threats, you first have to understand the architecture of internal controls to prevent fraud. This isn't a rigid set of rules but an interconnected system designed to manage the human factor in your organization. When these components work together, they create layers of defense. When one fails, the entire structure is exposed to massive liability and business impact.

At its heart, a strong internal control system is built on five essential pillars. Each one addresses a different angle of risk, from the cultural tone set by leadership down to the specific actions taken to safeguard assets. Understanding these pillars is the first step toward spotting the weak points in your current processes—and seeing where modern, AI-driven solutions can step in to provide critical, preventive support.

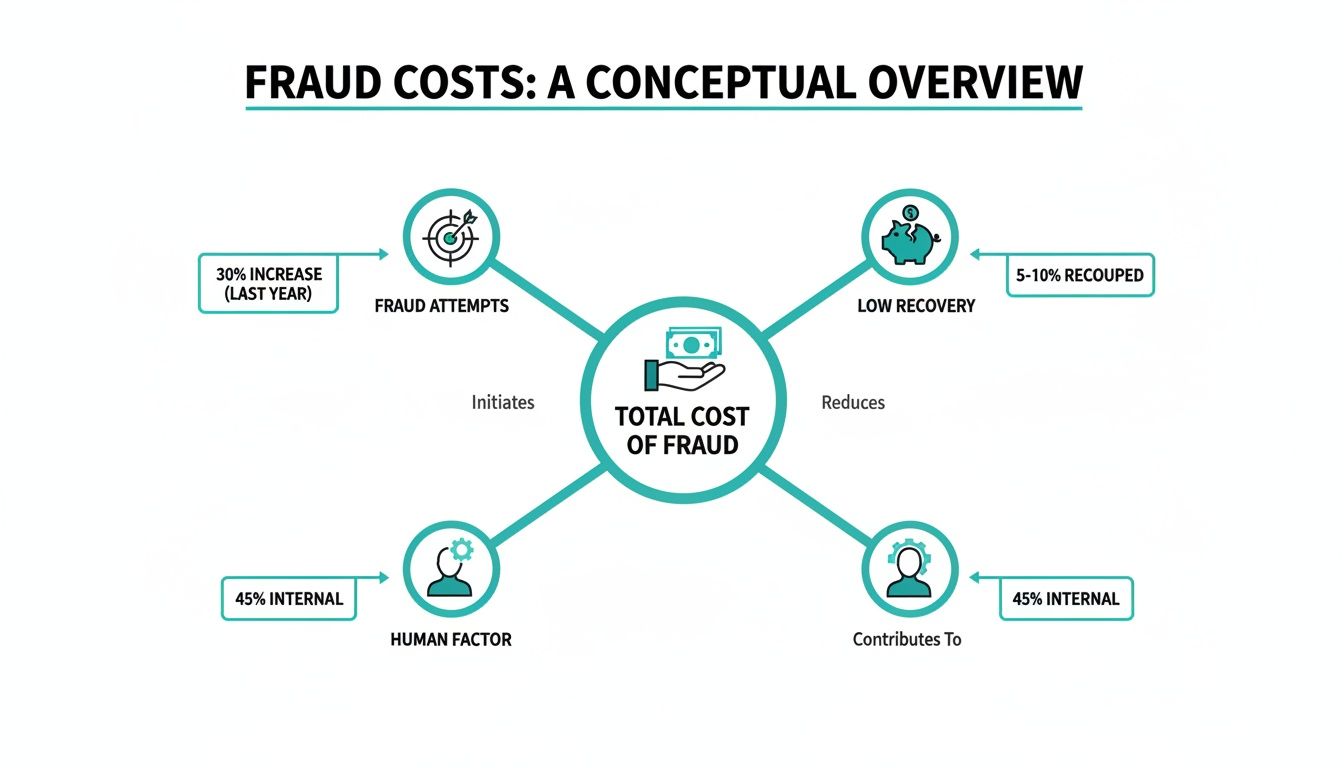

This diagram illustrates the main cost centers of fraud. It's not just one thing; it's a perfect storm of frequent attempts, low recovery rates, and the unpredictable human element driving it all.

What this shows is that fraud's true impact is a mix of direct financial loss and the constant threat posed by human vulnerabilities. This is exactly why robust, well-designed controls are absolutely essential for governance and reputation protection.

The Five Pillars Of Internal Control

A widely recognized framework breaks down internal controls into five distinct but deeply related components. Let's walk through each one with practical examples to see how they fit together.

This table gives a quick rundown of the five core components that form a traditional internal control framework, highlighting how each one contributes to preventing fraud.

Control Component | Primary Function |

|---|---|

Control Environment | Establishes the organization's ethical tone and commitment to integrity, starting from the top. |

Risk Assessment | Proactively identifies, analyzes, and manages specific fraud risks the organization faces. |

Control Activities | Implements specific policies and procedures designed to mitigate the risks identified. |

Information & Communication | Ensures clear, consistent communication of roles, responsibilities, and control policies across the organization. |

Monitoring Activities | Continuously assesses and evaluates the effectiveness of the control system over time. |

Each pillar builds on the others. A weakness in one can easily undermine the strength of the entire system, which is why a holistic, proactive view is so important.

Control Environment: This is the foundation—the "tone at the top." It’s about your organization's ethical values, management's philosophy, and the overall commitment to integrity. In a weak control environment where ethical shortcuts are tolerated, every other control is less effective.

Risk Assessment: This involves identifying and analyzing the specific human-factor risks your business faces. It’s an ongoing process of asking, "Where are we vulnerable?" A thorough fraud risk assessment is vital for pinpointing exposures, from financial statement manipulation to asset misappropriation.

Control Activities: These are the specific policies and procedures implemented to mitigate identified risks. Think of them as the practical actions your teams take to prevent fraud, like requiring dual authorization for payments or segregating accounting duties.

Information and Communication: For controls to work, information must flow effectively across the organization. This means clear communication about policies, roles, and responsibilities, as well as secure channels for reporting concerns.

Monitoring: Controls are not "set it and forget it." Monitoring involves regularly checking the effectiveness of your internal controls over time. This can be done through ongoing activities or separate formal evaluations.

Where Traditional Controls Fall Short

While these pillars provide a solid theoretical framework, their real-world effectiveness depends entirely on human execution. This is where traditional, manual systems break down, creating opportunities for internal threats that are incredibly hard to detect until it's far too late.

The most common failure point is a heavy reliance on manual processes vulnerable to human error, oversight, or deliberate override. For some guidance on building stronger defenses, especially in high-risk environments, check out these 10 ecommerce fraud prevention best practices.

A control system that looks perfect on paper can be rendered useless by a single employee with the authority to both approve a payment and reconcile the account. Without automated, ethical, and non-intrusive checks and balances, the system's integrity rests on flawed human judgment.

Consider these common vulnerabilities:

Collusion: When two or more employees collaborate, they can easily bypass fundamental controls like segregation of duties.

Management Override: Senior leaders can sometimes override established controls, creating a massive, top-down risk that undermines governance.

Human Error: Simple mistakes, such as data entry errors, can create unintentional gaps that a motivated individual can easily exploit.

These weaknesses don't mean the framework is flawed; they prove its implementation requires a more advanced, AI-driven approach. The clear limitations of manual oversight create a compelling business case for integrating technology that can monitor for risk signals continuously and ethically—augmenting human capabilities without resorting to invasive surveillance.

Why Reactive Systems Fail to Protect Your Business

Most companies remain stuck in a reactive posture when it comes to internal threats. They rely on traditional internal controls to prevent fraud, but these systems often act more like a historical record of a disaster than a protective shield. By the time a reactive investigation begins, the money is gone, operations are disrupted, and the company's reputation is at risk. This entire approach is fundamentally broken because it focuses on reacting to wrongdoing after the fact—a strategy that consistently proves to be too little, too late.

The core problem is that reactive systems are designed to analyze past events. This includes manual audits, forensic accounting, and whistleblower hotlines. While these tools have a place, they are not preventive. They are expensive, slow, and can foster a culture of suspicion. The focus shifts from proactive risk mitigation to a costly, disruptive search for evidence after the damage is done.

This obsession with looking backward leaves businesses perpetually exposed to modern, complex insider threats. A determined individual can often exploit gaps in manual processes for months, or even years, before anyone notices, leading to catastrophic losses that are almost never fully recovered.

The High Cost of Post-Incident Forensics

When fraud is finally discovered, the initial financial loss is just the beginning. The subsequent investigation triggers a cascade of secondary costs that can cripple an organization, creating massive business impact. These expenses include staggering legal fees, regulatory fines, and the immense operational disruption from pulling key people into forensic reviews. The entire process is a massive drain on resources that should have been invested in prevention.

The total damage includes:

Direct Financial Loss: The money or assets that were stolen.

Investigation Costs: Fees for forensic accountants, legal counsel, and specialized investigators.

Operational Disruption: Diverting management and employee time away from core business functions to assist with the investigation.

Reputational Damage: Loss of trust from clients, investors, and the public, which can have devastating long-term financial consequences and liability.

Waiting to act until after fraud is discovered is a guaranteed path to value destruction. The true cost of reactive investigations isn't just the money you lose; it's the trust, time, and operational stability you can never fully get back.

Understanding the full financial and operational hit is crucial. For a deeper analysis, you can explore the true cost of reactive investigations in our detailed article. The conclusion is clear: investing in prevention is exponentially more cost-effective than funding a clean-up operation.

The Legal and Ethical Pitfalls of Surveillance

In a misguided attempt to become more proactive, some organizations turn to traditional surveillance and employee monitoring systems. This is a critical mistake. These methods fail to identify the root causes of fraud and introduce severe legal and ethical problems. Invasive surveillance creates a toxic culture, treating all employees like potential suspects rather than valued partners.

This approach is particularly dangerous in the United States, where regulations like the Employee Polygraph Protection Act (EPPA) place strict limits on any method that could be perceived as coercive or intrusive. Using technology that functions like a "lie detector" or secretly monitors employee activity exposes a company to serious legal liability, undermining the very security it aims to create.

These surveillance-based systems are not the solution for today's insider risk landscape. They focus on policing behavior rather than understanding and mitigating the underlying human-factor risks that lead to fraud. An ethical, non-intrusive approach is not just a moral imperative—it's the only legally sound and effective strategy for sustainable risk prevention.

The New Standard: AI-Powered Preventive Risk Management

Traditional internal controls to prevent fraud are struggling to keep pace. The old model of quarterly audits and random spot-checks is too slow and narrow for today's dynamic business environment. By the time these methods uncover a problem, the damage is already done.

This reality is forcing a major shift toward a new standard in risk management, one driven by AI and built for proactive prevention, not reactive cleanup.

This is not about replacing people or implementing surveillance. It's about ethically identifying the subtle patterns and anomalies that signal potential insider risk long before it escalates into a full-blown fraud event. By integrating AI in accounting, companies can finally move beyond outdated manual oversight and adopt a more dynamic, intelligent posture to protect their financial integrity and corporate reputation.

From Manual Checks to Continuous Insight

The biggest weakness of manual controls is that they are merely a snapshot in time. An audit might happen once a quarter, but human-factor risk is a 24/7 problem. In contrast, an AI-driven human risk mitigation system works continuously, analyzing data streams to catch the faint signals a human reviewer would almost certainly miss.

This technology is not meant to replace human decision-makers; it is designed to arm them with better, more timely intelligence. It gives Compliance, HR, and Legal teams the critical, actionable insights they need to address potential conflicts of interest or ethical concerns with precision and confidence, strengthening governance.

The goal is not to police employees. It's to create an environment where the precursors to fraud—the subtle conflicts and ethical lapses—are identified and managed before they cause real business impact. This is the heart of true preventive risk management.

By focusing on objective risk signals instead of subjective judgments, these AI systems add a consistent and unbiased layer of defense that strengthens the entire control framework.

Ethical, Non-Intrusive, and EPPA-Aligned Prevention

One of the biggest concerns for decision-makers when adopting new risk technology is crossing ethical and legal lines. This is where the new standard of AI stands apart from older, invasive surveillance tools. A modern platform must be built on a foundation of respect for employee dignity and privacy, adhering strictly to regulations.

The most effective internal controls to prevent fraud are those that work ethically and transparently. A platform aligned with the Employee Polygraph Protection Act (EPPA) ensures your risk mitigation efforts never wander into dangerous legal territory. This means:

No Surveillance: The system does not monitor employee emails, communications, or daily keyboard strokes. It analyzes specific, risk-related data points with full transparency.

No "Lie Detection": It completely avoids any technology that attempts to assess psychological states, a practice that is strictly prohibited and legally perilous.

Focus on Prevention, Not Punishment: The insights are used to get ahead of risk, not to build cases against employees after the fact.

This ethical framework protects your organization from liability while building a culture of integrity. For a deeper look at how this works, you can read our guide on leveraging machine learning for fraud detection.

This isn't just a trend; it's rapidly becoming a regulatory expectation. Businesses globally are adopting AI for fraud prevention, with 52% already implementing or enhancing models to sharpen their risk-based decisions. As regulators push for stronger preventive measures, somewhere between 55% and 63% of firms are now deploying machine learning for detection, signaling a massive shift toward technology-driven controls.

Logical Commander's E-Commander and Risk-HR platforms embody this new standard. We deliver a non-intrusive, AI-based internal threat prevention system that protects both the company and its people before risk turns into damage.

Implementing Ethical Internal Controls with Advanced AI

Moving from theory to practice is where organizations build effective internal controls to prevent fraud. Adopting a modern, AI-driven framework isn’t just about new software; it’s about implementing a new standard of prevention—one that’s both powerful and ethical. This requires a platform capable of turning data into actionable risk intelligence without resorting to invasive methods.

That’s exactly what Logical Commander’s E-Commander and Risk-HR platforms were designed to do. They provide a tangible way to implement proactive, non-intrusive controls that align with today’s complex business and regulatory environments. This approach shifts your focus from chasing yesterday's problems to identifying and mitigating tomorrow's human-factor risks before they materialize.

Unifying Internal Risk Intelligence

One of the biggest failures of traditional controls is fragmentation. Risk data often lives in disconnected silos across HR, Compliance, Legal, and Security, making it nearly impossible to see the big picture of an internal threat. An employee’s conflict of interest might be noted in one system while a related compliance issue sits completely unnoticed in another.

The E-Commander platform solves this by creating a unified operational layer for internal risk management. It centralizes all your risk intelligence, providing a single, coherent view for every stakeholder. This breaks down departmental barriers and ensures your teams are working from the same set of facts, allowing for a coordinated and strategic response to potential threats.

By centralizing risk signals, organizations can finally connect the dots between seemingly unrelated events. This holistic view is the difference between overlooking a critical internal threat and proactively mitigating it before it can cause financial or reputational harm.

Ethically Identifying Integrity Risks

The true power of modern internal controls to prevent fraud lies in their ability to identify integrity risks early and, most importantly, ethically. This is where the Risk-HR module excels. It was purpose-built to analyze human-factor risks without ever crossing the line into surveillance or judgment-based assessments.

Risk-HR operates strictly within the guidelines of the Employee Polygraph Protection Act (EPPA). It does not monitor behavior or attempt to analyze psychological states. Instead, it identifies objective, verifiable risk indicators—like undisclosed conflicts of interest or patterns that point to potential misconduct—that warrant a closer, human-led review.

This system gives HR and Compliance leaders the tools for ethical insider threat detection, arming them with precise, actionable insights. You can learn more about this approach by exploring our guide on ethical insider threat detection solutions. It allows them to address concerns professionally and privately, reinforcing a culture of integrity rather than one of suspicion.

Driving Tangible Business Impact

Ultimately, the goal of any control system is to protect the business. The implementation of E-Commander and Risk-HR delivers measurable impact across several key areas:

Reduced Financial Losses: By identifying and mitigating human-factor risks before fraud occurs, the platform directly prevents the financial drain from theft, embezzlement, and other schemes.

Protected Corporate Reputation: Proactively managing integrity risks helps you avoid the public scandals and loss of trust that follow major compliance failures or fraud incidents.

Strengthened Governance: A centralized, AI-driven system provides leadership and boards with verifiable assurance that internal controls are operating effectively and consistently.

A Strategic Opportunity Through Our Partner Program

For B2B SaaS providers, consultants, and advisory firms, delivering this next-generation solution represents a significant strategic opportunity. The PartnerLC program is designed for allies who want to equip their clients with the new standard in preventive risk management.

By joining our partner ecosystem, you can offer a proven, EPPA-aligned platform that addresses a critical need for your clients, especially those in regulated industries. It’s a chance to move beyond offering theoretical advice and start delivering practical, AI-driven technology that hardens defenses against the most sophisticated internal threats.

Your Questions on Fraud Prevention Controls, Answered

When leaders in Compliance, HR, and Legal evaluate modern fraud prevention, critical questions always arise. The risk landscape has changed, and old reactive methods no longer suffice. You need answers that speak to the shift toward proactive, ethical, and technology-driven internal controls to prevent fraud.

This isn't about high-level theory. It's about providing the practical clarity needed to make informed decisions that protect your organization from liability and reputational damage. Let’s address how advanced systems work, integrate into existing workflows, and deliver strategic business value.

How Do AI Controls Differ from Traditional Surveillance?

This is the most important distinction. Traditional surveillance tools are invasive by design. They operate by monitoring employee activity—such as keystrokes, emails, or web browsing—in a broad, intrusive dragnet. This approach not only creates a culture of distrust but also puts your organization in serious legal jeopardy under regulations like the EPPA.

Advanced AI controls, like those in the Logical Commander platform, are built on a completely different, ethical philosophy. They are intentionally non-intrusive and focus on analyzing specific, objective risk signals, not policing employee behavior.

No Monitoring: The system does not track day-to-day employee activities. Period.

Focus on Integrity Risks: It is designed to identify verifiable conflicts of interest, ethical lapses, and other objective precursors to fraud.

EPPA-Aligned: The entire process is built to be fully compliant with labor laws, completely avoiding any methods that resemble lie detection or psychological evaluation.

Think of it this way: our AI is a surgical tool for risk identification, not a blunt instrument of surveillance. It delivers focused risk intelligence to your decision-makers without violating employee privacy or dignity.

Can These Controls Integrate with Our Existing Systems?

Absolutely. Integration is a core design principle of any modern risk platform. An advanced system for internal controls isn’t meant to rip and replace your existing compliance and HR infrastructure. It acts as a unifying operational layer that makes the tools you already use more effective.

The E-Commander platform, for instance, is built to centralize risk intelligence from disparate sources. This breaks down the information silos that so often allow internal threats to go unnoticed, creating a single, coherent view for your teams. It augments your current workflows by feeding in a new stream of actionable, preventive insights.

What Kind of ROI Can We Expect from Proactive Controls?

The return on investment for proactive internal controls to prevent fraud is measured in disasters averted and massive costs avoided. While reactive investigations rack up enormous bills for legal fees and forensic accounting, a preventive approach delivers its value by stopping fraud before it starts, protecting the bottom line and corporate reputation.

The financial incentive is huge. With consumer fraud losses recently exploding to over $12.5 billion—a staggering 25% jump in just one year—the cost of inaction is clear. Critically, only a third of organizations catch most fraud during the onboarding phase, leaving them exposed. It’s no surprise, then, that an overwhelming 87% of institutions confirm that their investments in fraud prevention deliver significant net savings. You can explore more insights on these fraud trends and their financial impact.

The ROI of prevention isn't just about the money you save from a single averted incident. It's about protecting brand reputation, maintaining investor confidence, and fostering a culture of integrity—assets that are priceless and fundamental to long-term business success.

Are These Systems Fully Automated or Do They Require Human Oversight?

Advanced AI systems are designed to augment human intelligence, not replace it. Your leaders in HR, Legal, and Compliance always remain in the driver's seat.

While the platform automates the heavy lifting of identifying potential risk signals, the final decision-making authority stays with your organization’s experts. The system acts as a powerful analytical assistant, flagging potential issues that warrant a closer, human-led review. It provides objective data and insights, but the context, interpretation, and subsequent action are entirely human responsibilities.

This "human-in-the-loop" model ensures that decisions are made with the necessary nuance and professional judgment, creating a powerful partnership between AI-driven analysis and experienced human oversight.

At Logical Commander, we provide the new standard for ethical, proactive internal threat management. Our AI-driven platform helps you identify and mitigate human-factor risks before they cause financial or reputational damage, all without invasive surveillance.

Ready to move from a reactive to a preventive strategy?

Learn more about our PartnerLC program for B2B SaaS providers

Contact our team to discuss an enterprise deployment